Introduction

Uganda is grappling with a housing deficit of 2.4 million units, a shortfall driven by rapid urbanization, demographic growth, and constrained public resources. In response, the government and private sector have launched a variety of initiatives to deliver affordable homes, aiming to bridge the gap between supply and demand. Central to these efforts is the National Housing and Construction Company (NHCC), Uganda’s primary state-owned residential developer, alongside commercial entities such as Habitat Uganda Limited and the Uganda Women’s Housing Association.

Policy Framework & Government Initiatives

- Housing Finance Bank (HFB) Products: To improve access to homeownership, HFB introduced low-cost mortgage products in 2023, featuring reduced interest rates (from 18% to 14%) and extended tenors up to 25 years. Despite this, uptake remains limited, with mortgage penetration stagnant at 1.6% of GDP due to stringent eligibility criteria and income documentation requirements.

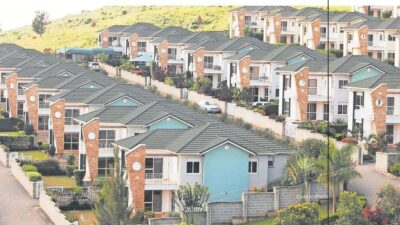

- NHCC Social Housing Projects: NHCC’s flagship pilot in Lubowa delivered 500 units in 2024 at a subsidized average cost of UGX 80 million per unit (USD 22,000). A subsequent phase targeting 2,000 units in Namanve is due for rollout in Q4 2025.

- Legal & Tax Incentives: Parliament passed amendments in 2023 providing tax holidays (five-year exemption) for developers investing in affordable housing zones. Additionally, Value Added Tax (VAT) on building materials for projects under UGX 100 million/unit was reduced from 18% to 5%.

Market Challenges

- Financing Barriers: Mortgages remain out of reach for many due to high down payments (20–30% of property value) and inadequate income verification for informal-sector workers, who constitute over 70% of Kampala’s workforce.

- Land Acquisition & Regulatory Delays: Developers report average lead times of 12–18 months to secure land titles, conduct environmental impact assessments, and obtain building permits—a process exacerbated by overlapping mandates across the Ministry of Lands and local councils.

- Infrastructure Deficits: Many affordable estates lack reliable water, sanitation, and road access, diminishing their attractiveness despite low capital costs.

Private Sector Innovations

- Slum Upgrading & Incremental Housing: NGOs like Shelter and Tony Blair Institute collaborate with local communities in Kisenyi to upgrade informal settlements, providing modular units and microfinance schemes for incremental construction.

- PropTech Solutions: Digital platforms—e.g., PriceHubble and M-Farm—are piloting mortgage eligibility scoring using mobile data, aiming to improve credit access for low-income earners by Q2 2025.

- Green Affordable Housing: Pilot projects in Jinja employ interlocking stabilized soil blocks and solar water heating, reducing construction costs by up to 20% and utility expenses by 30%.

Investor Implications

- High Demand, Low Supply: With waiting lists exceeding 10,000 applicants for NHCC estates, investors have a clear pipeline for high-volume, lower-margin projects.

- Risk Mitigation: Partnerships with microfinance institutions and digital credit-scoring firms can reduce default risks.

- ESG & Impact Investing: Affordable housing projects that integrate sustainability metrics (e.g., energy efficiency, community facilities) are attracting interest from international impact funds.

Conclusion & Outlook

While recent regulations and tech pilots signal progress against fraud, sustained efforts in enforcement, public education, and digital infrastructure are essential. By 2026, the combined impact of new laws and blockchain registries could significantly reduce fraud and bolster investor confidence.